Read this article in French German Italian Portuguese Spanish

Is the crane rental market booming? Exploring 2024’s global growth and regional trends

28 January 2025

In 2024, the global crane rental market experienced significant growth, driven by increased construction activities, infrastructure development, and industrial expansion across Europe, Asia, and the USA. Crane and Transport Briefing reports.

In Europe in particular, the market benefited from infrastructure upgrades and sustainable building initiatives which are being adopted by a large number of companies, while Asia-Pacific, particularly China and India, saw rapid expansion due to increased urbanisation and industrialisation.

Rental rates remained competitive, with a growing preference for renting over purchasing cranes due to cost-effectiveness and flexibility. This trend was evident across various regions.

Crane expectations

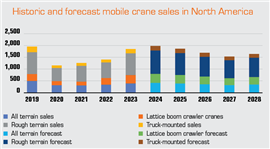

Specialist forecaster OffHighway Research was expecting about 7 per cent growth in crane sales in North America in 2024. (Image: OffHighway Research)

Specialist forecaster OffHighway Research was expecting about 7 per cent growth in crane sales in North America in 2024. (Image: OffHighway Research)

Specialist forecaster OffHighway Research’s managing director Chris Sleight states that crane sales in the USA continued to rise in 2024, despite a slowing growth in the construction market and falling sales of other types of construction equipment.

Construction activity took off during the pandemic, particularly the housebuilding sector where the stimulus of low interest rates and direct injections of cash from job protection schemes encouraged individuals to move to bigger properties or renovate their homes.

As far as the current cycle is concerned, the construction markets look to be topping-out in 2024. The one-off boosts that have been apparent from the various policies of the pandemic era look to have run their course, while residential construction is healthy, but probably as high as it is going to get. There may be a little more upward movement as interest rates come down over the next 12 to 18 months, but this is against the backdrop of a somewhat weak economic outlook in terms of GDP growth.

Election uncertainty

The other factor over the last year has been uncertainty in the run-up to the US election. It was clear in 2016 that many buying decisions were put off until after the election, which gave clarity to the country’s policy direction for the next four years. That was clearly the case over the course of 2024 in what was, even by the standards of recent election campaigns, something of an unusual and unpredictable chain of events. The combination of high interest rates and uncertainty ahead of the results certainly took its toll on the higher volume end of the construction equipment market.

The market for mobile cranes (all terrain, rough terrain, truck and crawler cranes) in North America continued to grow in 2024. Off-Highway Research was expecting about 7 % growth in sales for the year.

Mobile crane sales bucked the trend in the wider equipment market for several reasons. First, the high volume construction equipment types such as mini excavators and compact tracked loaders are particularly affected by housebuilding activity, which had something of a reset over 2023 and 2024. There was also some saturation in the market for these machine types following the boom years of the pandemic. In contrast, crane sales are more closely linked to infrastructure and non-residential building, which continued to rise in 2024.

A second factor is that it took the mobile crane industry a long time to get over the supply chain constraints of the pandemic years. Whereas sales of high volume construction machines soared to a series of record highs in the early 2020s, it was only in 2024 that sales of mobile cranes came back to their pre-Covid levels. It seems likely that 2024 will prove to be the high water mark for crane sales in the current cycle.

A modest decline can be expected in 2025 against a backdrop of fairly mediocre economic growth and construction markets that have topped-out.

European rebound

The European equipment rental industry is highly fragmented, with a large number of small players serving local or regional markets, and a smaller number of medium-sized to large players serving regional, national, and international customer bases, says International Rental News Editor Lewis Tyler. However, with the increasing professionalism of the trade, the rise in demand across end markets, and the growing need for investment, the industry has experienced a high degree of consolidation in recent years.

According to the European Rental Association (ERA) 2024 Market Report, the EU economy began to emerge after a period of stagnation. Growth was predicted to reach 1 per cent in 2024 and then rise to 1.6 % in 2025, after having plateaued at 0.4 % in 2023. Since the beginning of the 2024, inflation had returned to normal levels. At the same time, labour markets throughout Europe continued to be tight, with wages growing at a high rate.

Overall, in 2024, the European rental market normalised, undergoing a post Covid-19 rebound. Interest rates and general uncertainty directly affected the residential segment, which is suffering across the EU (albeit with relative importance for the rental industry).

In the coming years, EU investment via the National Recovery and Resilience Plan (NRRP) is expected to boost rental activity. According to the ERA report, the European rental market is projected to grow by 2.8 % in 2025, and 3.6 % in 2026, reflecting steady growth in the industry.

Central Europe and the UK are in the post-Covid normalisation phase. The market is forecast to soften in this year, apart from Ireland, which maintains a strong outlook driven by resilient housing demand and energy projects. France continues to see soft growth, and Germany experienced slight growth in 2024. Poland and Czech Republic faced fluctuations due to general uncertainty and limited growth drivers.

Finland and Sweden are experiencing downturns, with continued stagnation expected, with largely halted residential construction. Both countries anticipate a recovery in the second half of 2025, driven by public investments and energy-related projects. Denmark and the Netherlands continue to rebound. In 2024, the equipment rental markets in Italy, Portugal, and Spain were tracking steady growth.

The European rental market has experienced a steady increase in its rental penetration rate over the past years, reflecting the growing preference of customers to rent rather than buy equipment and tools. Renting offers access to modern equipment, flexibility, and cost-efficiency, as it reduces capital expenditure requirements, fixed costs of ownership, and residual value risk while allowing customers to adapt to changing demand and project requirements.

Asian moves

Photo: Adobe Stock

Photo: Adobe Stock

The dramatic growth of AWP rental fleets in China – 700,000 machines and counting – has left the market exposed, with the slowdown of the Chinese economy leading to lower rental prices and oversupply, writes Rental Briefing’s Murray Pollok.

That in turn has led many Chinese rental companies consider moving outside of China, with Shanghai-based CDHorizon being the most prominent example.

Rental Briefing understands that CDHorizon now has more than 1100 machines in the UAE, and it is also opening in Saudi Arabia. Closer to home, it already has rental operations in Malaysia, Indonesia, Vietnam and Thailand.

Rental prices in China have declined by more than 20 % compared to 2023, said Li Ying, general manager of Liugong Access, speaking at the 11th International Rental Conference (IRC); “The sharp drop in rental prices has caused widespread defaults and financial stress. It’s nearly impossible for companies to recover costs or achieve profitability under these conditions.”

The downturn has forced many rental company owners to reassess their strategies. “Just two years ago, many of these [new rental] leaders were optimistic and confident,” he said. “Now, with the market shrinking, they are questioning their paths and facing significant self-doubt.”

Jimmy Wang, founder and CEO of rental firm China Construction Bright Future (CCBF), said a shift to overseas rental markets was one consequence of the domestic squeeze; “The search for margins is driving the overseas diversification.”

He said the Middle East was the first priority target market, followed by South East Asia, and finally countries associated with China’s Belt and Road project, which includes nations such as Pakistan, Kazakhstan, Sri Lanka and Laos.

Giving the OEM perspective was Dawei He, international sales and marketing director at Sinoboom. He said Chinese manufacturers had to shift from volume-based to a “value-based” strategy; “Not copy-cat products to grab market share at the expense of margins.”

At the same time, aftermarket services need to improve; “I strongly recommend all Chinese manufacturers – including Sinoboom – to pay more attention to the aftermarket. If you do, you are more likely to succeed.”

What was interesting about his comments is that they included a recognition about the role of Chinese OEMs in the oversupply of machines in the market; “If more production capacity is released [in China], it will jeopardise the whole market.

“We need to get rid of our dependence on scale. We need to rely more on developing new use cases, new technology. It will create a healthier ecosystem.”

American revival

The equipment rental industry in the USA was predicted to reach $79.2 billion in 2024, according to the latest reports from the American Rental Association (ARA).

Tom Doyle, ARA vice president of program development, said, “The 2024 ARA forecast, through the lens of our exclusive rental revenue model and survey results gathered from members, confirmed the continuation of a growing rental industry.”

Scott Hazelton, managing director at S&P Global, added, “There was no serious bust, thus, there is no serious boom. The outlook remained steady, and inflation was falling. Growth rates were expected to tail off in future years, with growth of 3.8 % in 2025 and 3.1 % in 2026.”

According to Jeff Vance, senior vice president of operations services at Sunstate Equipment, the S&P forecasts aligned with the company’s own, which predicted a softer winter and spring than usual and softening used equipment prices.

In Canada, equipment rental revenue was projected to grow by 7.2 % in 2024, totalling $5.79 billion.

Darryl Cooper, president of Cooper Equipment Rentals, noted, “Our experience mirrored what ARA reported. Despite headwinds in the residential market, revenues were up, with western Canada stronger than eastern Canada.”

In terms of the supply chain, Sunstate observed a loosening, with fleet and parts becoming easier to obtain.

Additionally, Vance reported that new vendors had been introduced into the marketplace with new technology, saying, “We conducted a lot of investigation into electrification. The power grid was always a topic in our minds. But more electrification was coming, so we had to be prepared to service our customers in those ways.”

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM